Three Years After Recession a Long-Tail Emerges

As Tolstoy famously said, “The strongest of all warriors are these two – time and patience.” On the tail end of fighting through the longest recession in the memories of most alive today, time has brought about many changes. In the first quarter of 2009, more than 2 million jobs disappeared. On March 6, 2009, the Dow closed at 6626 and by the end of the year unemployment had risen to 10 percent. In the first quarter of 2012, more than 600,000 jobs were added, the Dow reached over 13000 points and unemployment nearly fell below 8 percent.

“A tightening labor market, though, isn’t the entire story. While 3.7 percent of professionals may be out of a job today, as you layer on specific qualifications, backgrounds, or years of experience, the number of candidates actively seeking a job can drop to virtually zero,” notes Romaine.

“A tightening labor market, though, isn’t the entire story. While 3.7 percent of professionals may be out of a job today, as you layer on specific qualifications, backgrounds, or years of experience, the number of candidates actively seeking a job can drop to virtually zero,” notes Romaine.News/Insights

Job Market/Industry News

Job Market/Industry News

The Power of Emotional Intelligence in the Doctor-Patient Relationship

Jun 5, 2023

“Physician leaders who are able to exhibit high degrees of emotional intelligence (EI), particularly in how they manage their own emotions and react to the emotions of other...

Hiring

Hiring

Where Are All the Optometrists and Ophthalmologists?

Oct 27, 2021

The market for Optometry and Ophthalmology talent has always been competitive. Several factors have combined to make what was already a tight market even more challenging. T...

Job Market/Industry News

Job Market/Industry News

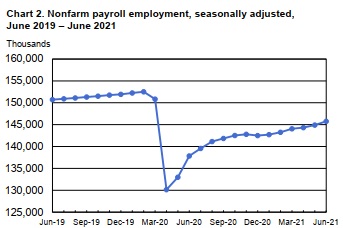

Employment Situation Report – June 2021

Jul 2, 2021

Summary of the Bureau of Labor Statistics Monthly Employment Situation Report – June 2021 Continuing a six month increase in job growth, the U.S. Bureau of Labor Stat...

Hiring

Hiring

Are You Ready for What’s Next?

Mar 24, 2021

Everyone is trying to understand what’s coming next in a post-COVID-19 world. While we have no special foresight into the future of the pandemic, we can tell you what we hav...

Job Market/Industry News

Job Market/Industry News

Employment Situation Report – February 2021

Mar 10, 2021

Summary of the Bureau of Labor Statistics Monthly Employment Situation Report The U.S. Bureau of Labor Statistics (BLS) today reported total nonfarm payroll employment incr...

Job Market/Industry News

Employment Situation Report – January 2021

Feb 11, 2021

Summary of the Bureau of Labor Statistics Monthly Employment Situation Report The January job gain of 49,000 was in-line with most analysts’ expectations and represented ...

Job Market/Industry News

Employment Situation Report – December 2020

Jan 14, 2021

Summary of the Bureau of Labor Statistics Monthly Employment Situation Report Total nonfarm payroll employment declined by 140,000 in December, well below the consensus forec...

Job Market/Industry News

Employment Summary for November 2020

Dec 7, 2020

Summary of the Bureau of Labor Statistics Monthly Employment Situation Report The U.S. economy added 245,000 non-farm jobs in November, below the 410,...

Job Market/Industry News

Employment Summary for October 2020

Nov 20, 2020

The U.S. economy added 638,000 non-farm jobs in October, above the 530,000-job growth expected by economists. The unemployment rate declined to 6.6 percent. October is the six...

Job Market/Industry News

Employment Summary for September 2020

Oct 5, 2020

Summary of the Bureau of Labor Statistics Monthly Employment Situation Report The U.S. economy added 661,000 non-farm jobs in September, below the 800,000 job growth expected...